Canada Gazette, Part I, Volume 151, Number 21: Regulations Respecting Reduction in the Release of Methane and Certain Volatile Organic Compounds (Upstream Oil and Gas Sector)

Mai 27, 2017

- Statutory authority

- Canadian Environmental Protection Act, 1999

- Sponsoring departments

- Department of the Environment

Department of Health

- Department of the Environment

REGULATORY IMPACT ANALYSIS STATEMENT

(This statement is not part of the Regulations.)

Executive summary

Issues: Greenhouse gas (GHG) emissions are contributing to a global warming trend that is associated with climate change. Oil and gas facilities account for 26% of Canada's total GHG emissions. These facilities are also Canada's largest emitters of methane, a potent GHG with a global warming potential 25 times that of carbon dioxide (CO2).

Description: The proposed Regulations Respecting Reduction in the Release of Methane and Certain Volatile Organic Compounds (Upstream Oil and Gas Sector) [the proposed Regulations] would introduce control measures (facility and equipment level standards) to reduce fugitive and venting emissions of hydrocarbons, including methane, from the oil and gas sector.

Cost-benefit statement: Between 2018 and 2035, the cumulative GHG emission reductions attributable to the proposed Regulations are estimated to be approximately 282 megatonnes of carbon dioxide equivalent (Mt CO2e). Avoided climate change damages associated with these reductions are valued at $13.4 billion. The total cost of the proposed Regulations is estimated to be $3.3 billion, which would be offset in part by the recovery of 663 petajoules (PJ) (see footnote 1) of natural gas, with a market value of $1.6 billion, resulting in expected net benefits of $11.7 billion.

“One-for-One” Rule and small business lens: The proposed Regulations would result in an increase in average annual administrative burden costs of around $1.1 million, or about $1,100 per business. The proposed Regulations are therefore considered to be an “IN” under the Government of Canada's “One-for-One” Rule.

The small business lens applies, and various flexibilities have been incorporated into the proposed Regulations to address the concerns of small businesses. These flexibilities are expected to reduce the cost of the proposal for small businesses by $56 million, or $120,000 per small business, over 18 years. The proposed Regulations would result in cumulative costs of about $14 million for small businesses, or $30,000 per small business.

Domestic and international coordination and cooperation: The proposed Regulations would deliver on the Prime Minister's March 2016 commitment to reduce emissions of methane from the oil and gas sector by 40% to 45% below 2012 levels by 2025 and would be consistent with Canada's commitment in the United States–Canada Joint Statement on Climate, Energy, and Arctic Leadership; the Paris Agreement; and the Leaders' Statement on a North American Climate, Clean Energy, and Environment Partnership. Harmonization with provincial measures has been incorporated into the proposed Regulations to the extent possible.

Background

Methane (CH4) is a hydrocarbon that is the main component of natural gas. In its pure state, methane is a colourless, odourless flammable gas and is considered a toxic substance listed under Schedule 1 of the Canadian Environmental Protection Act, 1999 (CEPA). It is also a greenhouse gas (GHG) with a global warming potential 25 times greater than that of carbon dioxide (CO2). Oil and gas facilities account for 26% of Canada's total GHG emissions and are Canada's largest industrial emitters of methane. The majority of these emissions are released by fugitive (unintentional releases) and venting (intentional releases) sources.

Historical and current GHG emissions are causing the global average surface temperature to increase, leading to climatic changes such as the increased frequency and severity of extreme weather events. The impacts of climate change are already becoming evident. These include thawing permafrost, eroding coastlines and rising sea levels. These impacts are expected to worsen as temperatures rise. Climate change is of major concern for society due to impacts on natural habitats, agriculture and food supplies, infrastructure, and low-lying and coastal communities. (see footnote 2)

The Government of Canada is committed to taking action on climate change. At the United Nations Framework Convention on Climate Change (UNFCCC) conference in December 2015, the international community, including Canada, reached the Paris Agreement, an accord intended to reduce global GHG emissions in order to limit the rise in global average temperature to less than 2 °C above pre-industrial levels and to pursue efforts to limit the temperature increase to 1.5 °C. As part of the Paris Agreement, Canada pledged to reduce national GHG emissions by 30% below 2005 levels by 2030, (see footnote 3) including a commitment to develop regulations to address methane emissions from the oil and gas sector. (see footnote 4)

In March 2016, Canada and the United States issued the Joint Statement on Climate, Energy, and Arctic Leadership and have committed to working together to implement their respective commitments under the Paris Agreement. Building on a history of joint activity to reduce air emissions, Canada and the United States agreed to take action to reduce methane emissions from the oil and gas sector, the world's largest industrial methane source. Both countries adopted a target to reduce emissions of methane from their oil and gas sectors by 40% to 45% below 2012 levels by 2025. (see footnote 5) In June 2016, Mexico joined Canada and the United States and committed to the target as well under the Leaders' Statement on a North American Climate, Clean Energy, and Environment Partnership. To achieve this target, Canada, the United States and Mexico committed to introducing or expanding federal regulations to reduce methane emissions from oil and gas facilities. (see footnote 6)

Hydrocarbons, natural gas and crude oil

Natural gas and crude oil are blends of various hydrocarbons extracted from deposits or reservoirs found beneath the surface of the earth and ocean floors. Hydrocarbons are molecules in various combinations of carbon and hydrogen that can occur as gases at atmospheric pressure and liquids under higher pressures. (see footnote 7) Crude oil facilities extract liquid hydrocarbons, which can then be refined into gasoline, diesel, fuel oils, kerosene, jet fuel, asphalt, road oil and a variety of other fuels. Natural gas is a mixture consisting mostly of methane and is often used as fuel or to make materials and chemicals. (see footnote 8) Natural gas facilities extract, process and transport hydrocarbon gas. Natural gas and crude oil can often be found in association with each other in the same reservoir. As a result, crude oil facilities may also produce some natural gas, while natural gas facilities may also extract certain liquid hydrocarbons.

Emission sources in the oil and gas sector

The oil and gas industry encompasses many activities, from “upstream” activities, such as exploration, drilling, production and field processing, to “downstream” activities, such as petroleum refining and bulk storage and distribution of refined petroleum products. In 2012, close to 90% of methane emissions from the oil and gas sector came from upstream activities. Major sources of hydrocarbon emissions from the oil and gas sector are described below.

Facility production venting: General venting emissions from oil and gas facilities occur during the production process. This includes emissions from storage tanks and wellhead casings. Methane has a global warming potential 25 times that of carbon dioxide and is a short-lived climate pollutant. Releasing methane into the atmosphere has significant climate change consequences in comparison to flaring (burning) methane. This is because flaring converts methane to carbon dioxide, which has a much lower global warming potential.

Fugitive equipment leaks: Fugitive leaks may occur as a result of poor maintenance or regular wear and tear of equipment at all stages of production and processing of oil and gas. Leaks of gas or vapour may originate from components on equipment piping such as valves, flanges, and connectors.

Well completion by hydraulic fracturing: Well completion is the process of making a new well ready for production or stimulating an existing well to improve production, often through the use of hydraulic fracturing (or refracturing) techniques. After hydraulic fracturing, the well bore and formation must be cleaned of debris and fracturing fluid, a process that involves sending the well flowback material to an open pit or tank for disposal. Any natural gas that is extracted along with the flowback material during this process could be vented into the atmosphere.

Pneumatic controllers and pumps: Pneumatic controllers are used in the oil and gas industry to measure and control parameters in the operations process, such as temperature, pressure, flow or liquid level. Pneumatic pumps are used to pump chemicals. Pneumatic instrumentation is commonly used by the industry due to its simplicity and reliability. A common practice is to use high-pressure field gas (see footnote 9) to operate these pneumatic devices. In gas-driven pneumatic devices, natural gas may be released into the atmosphere with every instrument actuation, or continuously from the device.

Compressors: Compressors are mechanical devices that increase the pressure of natural gas and allow it to be transported from the well site where it is produced, through a system of smaller flow lines and field processing facilities, and into the larger pipeline system for eventual delivery to the consumer. Compressors can vent gas through regular use and wear and tear of internal components.

Domestic emission control measures

Presently, there are no federal regulations established to regulate GHG emissions from the upstream oil and gas sector. There are some provincial instruments in place, particularly in British Columbia, Alberta and Saskatchewan, where the majority of onshore oil and gas activities are occurring. The Canadian Association of Petroleum Producers (CAPP) also has guidelines for flaring. However, these provincial instruments are not entirely consistent across jurisdictions and do not cover all sources of fugitive and venting emissions.

In British Columbia, the Flaring and Venting Reduction Guideline applies to the flaring, incineration and venting of natural gas at well sites, facilities and pipelines. Other requirements also exist for industry reporting of GHG emissions. While the province has a carbon tax in place, it does not apply to venting or fugitive emission sources from the oil and gas sector.

Alberta's Directive 060 imposes requirements for incinerating and venting in the province at all petroleum industry wells and facilities. Venting reduction through solution gas (see footnote 10) conservation or gas flaring is based on reported vented emissions from the entire facility. Reported vented volumes include volumes from process vents, tank vents, and surface casing vents, but exclude venting from pneumatic instrumentation and pumps. Alberta also has in place the Specified Gas Emitters Regulation (SGER), which requires facilities that emit over a certain threshold to reduce emission intensity.

Saskatchewan's Directive S-10 sets out requirements for the reduction of flaring and venting of associated gas, applicable to oil wells, associated gas processing plants, and any wells that vent, flare, or incinerate associated gas. Likewise, Saskatchewan's Directive S-20 provides performance requirements, and specification for equipment spacing and setback distance specifications for oil and gas flaring and incineration, applicable to licensed wells and facilities. The S-10 and S-20 directives set out the main provincial requirements governing venting and flaring emissions in Saskatchewan.

The Canadian Standards Association (CSA) develops voluntary codes, and some of these standards apply to the oil and gas sector. The Fugitive Emissions and Venting code specifies criteria to address fugitive and vented emissions from point sources from pipelines, wells and facilities in the upstream oil and gas sector. These standards specify criteria to develop emission reduction practices and programs.

International emission control measures

In April 2012, the United States Environmental Protection Agency (U.S. EPA) issued regulations under the Clean Air Act to reduce air pollution from the oil and natural gas industry. These new source performance standards (NSPS) included the first U.S. federal air standards for well completions at natural gas wells that are hydraulically fractured, new and modified tank emissions, pneumatic controllers at and between wellheads and natural gas processing plants, new and modified compressors and leak detection and repair (LDAR) programs for new and modified natural gas processing facilities.

The U.S. EPA updated the NSPS in 2016 to focus on the reduction of methane and volatile organic compound (VOC) emissions from new, reconstructed and modified oil and gas facilities. These updates added requirements to well completions to cover oil wells, extended pneumatic requirements to apply to gas transmission and to target methane, added methane requirements, extended applications to pipelines, extended LDAR to target methane specifically, and to apply to fugitive emissions from well sites, gas plants and compressor stations. The U.S. performance standards do not currently apply to existing facilities; however, they have been in place since 2016.

Issues

GHGs are a major contributor to climate change. The largest source of GHG emissions in Canada is the extraction and processing of fossil fuels. The latest emissions data available indicate that GHG emissions from production and processing activities in the oil and gas sector in Canada were 192 Mt in 2014, accounting for 26% of total GHG emissions. (see footnote 11)

Without immediate action, it is expected that fugitive and venting methane emissions from the oil and gas sector in Canada will continue to be released at high levels of about 45 Mt CO2e per year between 2012 and 2035.

Objectives

The Government of Canada has committed to undertake ambitious efforts to combat climate change, including international commitments under the United Nations Framework Convention on Climate Change (Paris Agreement and Copenhagen Agreement), and domestic commitments under the Pan-Canadian Framework on Clean Growth and Climate Change.

The objective of the proposed Regulations Respecting Reduction in the Release of Methane and Certain Volatile Organic Compounds (Upstream Oil and Gas Sector) [the proposed Regulations] is to achieve significant reductions in GHG emissions, through reductions in fugitive and venting emissions of hydrocarbons from the upstream oil and gas sector.

Description

The proposed Regulations would impose both general requirements and requirements that depend on a facility producing and receiving at least 60 000 m3 of hydrogen gas in a year. The requirements relate to production processes and equipment and have the effect of reducing the emission of methane and the targeted VOCs from the upstream oil and gas sector.

- — Facility production venting: Upstream oil and gas facilities would be required to limit vented volumes of hydrocarbons to 250 m3 per month as of January 1, 2023. These facilities would need to capture the gas and either use it on site, reinject it underground, send it to a sales pipeline, or route it to a flare. Facilities that vent less than 40 000 m3 of gas per year without destroying or selling any would not be required to destroy or conserve it.

- — Leak detection and repair: Upstream oil and gas facilities, except single wellheads, would be required to implement leak detection and repair (LDAR) programs as of January 1, 2020. Regular inspections would be required three times per year, and corrective action would be required if leaks are discovered. Leaks would need to be repaired within 30 days, if repairs are possible without shutting down the equipment. If repairs are not possible without shutting down the equipment, the facility operator would be required to schedule a shutdown to take corrective action before the volume of gas from the leak is larger than the volume of gas that would be released by shutting down the equipment. If the facility is located offshore and the equipment cannot be repaired while operating, corrective action would need to be taken within 365 days.

- — Well completion by hydraulic fracturing: These sites would be required to conserve or destroy gas instead of venting as of January 1, 2020. This standard would not apply to British Columbia or Alberta, where existing provincial measures cover these activities.

- — Pneumatic controllers: Controllers at facilities with a total compressor power rating of at least 745 kilowatts (kW) would be prohibited from emitting hydrocarbon gas as of January 1, 2023. Other facilities would be required to use low-emitting pneumatic controllers.

- — Pneumatic pumps: Pumps would be prohibited from emitting hydrocarbon gas or be equipped with an emissions control device at facilities where liquid pumping exceeds 20 L per day of liquid as of January 1, 2023. Permits for pneumatic pumps would be available when it is technically or economically infeasible for a facility to comply.

- — Compressors: Measurement of the flow rate of hydrocarbon emissions would be required from sealing systems, at least once per year, as of January 1, 2020. Corrective action would be required if those emissions exceed 0.023 m3 per minute for reciprocating compressors and 0.17 m3 per minute for centrifugal compressors. All new compressors installed would be required to capture gas from sealing systems.

All upstream oil and gas facilities would also be required to register and keep records in order to demonstrate compliance with the proposed Regulations. Facilities would also be required to submit reports at the request of the Minister of the Environment (the Minister).

Designation Regulations

The Regulations Designating Regulatory Provisions for Purposes of Enforcement (Canadian Environmental Protection Act, 1999) [the Designation Regulations] designate various regulatory provisions from CEPA regulations that set out an increased fine range following a conviction for an offence involving harm or risk of harm to the environment, or obstruction of authority. The proposed Regulations would be listed in the Designation Regulations, which would need to be amended to reflect the addition of new offences pertaining to the proposed standards.

Regulatory and non-regulatory options considered

In consideration of how to address the public policy issue, the Department of the Environment (the Department) considered five options: maintaining the status quo, using voluntary instruments, implementing a market-based approach, implementing regulatory emission control requirements that are closely aligned with the U.S. NSPS, or implementing Canada-specific regulatory emission control requirements.

Status quo approach

While British Columbia, Alberta and Saskatchewan have measures to address venting methane emissions, there is no federal requirement in Canada to reduce GHG emissions from existing upstream oil and gas facilities. These provinces currently have some instruments in place for some aspects of the upstream oil and gas sector, such as British Columbia's Flaring and Venting Reduction Guideline, Alberta's Directive 060 and Saskatchewan's directives S-10 and S-20. However, these instruments are not consistent across jurisdictions and do not cover all sources of emissions.

For these reasons, current and announced provincial measures would not alone deliver significant and achievable reductions in GHG emissions from the oil and gas sector, and may compromise Canada's ability to meet its international commitments. Therefore, maintaining the status quo was not an acceptable option.

Voluntary approach

Voluntary instruments, such as pollution prevention plans, environmental release guidelines, and codes of practice, have been considered as options for methane mitigation. Voluntary instruments provide greater flexibility for stakeholders in meeting the objectives of the policy but also require a large degree of stakeholder participation and support.

The large number and diversity of facilities in the upstream oil and gas sector make it difficult to arrive at voluntary goals that provide assurance of significant emission reductions. Uncertainty regarding buy-in by competitors under a voluntary measure may cause reluctance by firms to participate. While a voluntary program may result in some emission reductions, given its non-enforceable nature, it would not likely amount to the emission reductions to meet Canada's GHG targets. Voluntary approaches were ultimately rejected for these reasons.

Market-based approach

In October 2016, the Prime Minister announced a plan on pricing carbon pollution that would set a floor price for carbon pollution across Canada. However, fugitive and venting emissions are often from dispersed sources of emissions from a large number of mostly small facilities, which are unlikely to have adequate quantification protocols for tracking emissions. In fact, existing Canadian carbon pricing systems in British Columbia, Ontario and Quebec do not cover these emissions since the facilities do not meet the policy threshold. Therefore, a market-based approach was not considered sufficient to address fugitive emissions and venting releases of methane in the oil and gas sector.

Regulatory approach — Canada–United States alignment (new source performance standards)

A regulatory approach, designed to align closely with the current U.S. approach (NSPS) was considered. However, such an approach would not be consistent with existing provincial measures, resulting in misalignment within Canada; would not capture unique Canadian emission sources such as heavy oil; would impose substantial, unnecessary administrative burden on regulated parties that would be inconsistent with commitments in Canada's Cabinet Directive on Regulatory Management to control the administrative burden of regulations on business; and, would not initially cover a significant portion of existing facilities, making it difficult to meet the reduction targets announced by the Prime Minister (see footnote 12) in 2016. For these reasons, close alignment with the U.S. NSPS was rejected.

Regulatory approach under CEPA

The Government of Canada is committed to reducing methane and GHG emissions in the atmosphere in light of Canada's international agreements. The implementation of a regulation made under CEPA is considered a primary instrument to achieve this goal as it is very likely to ensure that emission reductions are achieved. This approach ensures that hydrocarbon emissions, including methane, are controlled and reduced from sources in a consistent fashion across Canada from similar sources in the upstream oil and gas industry.

The proposed Regulations would create clear and consistent performance standards across the country. CEPA allows for flexibility via equivalency agreements with interested provinces and territories, as long as the requirements of CEPA are met, which can enable these jurisdictions to be front-line regulators where they have legally binding regimes that produce equal or better environmental outcomes.

The proposed Regulations are based on current U.S. source-by-source rules that apply to new and modified oil and gas facilities, which were finalized in 2012 and 2016, with modifications to reflect Canadian conditions (including existing requirements in various Canadian jurisdictions) and input from stakeholders. The proposed Regulations would exempt the provinces of British Columbia and Alberta from the well completion by hydraulic fracturing requirements. These provinces already have regulatory measures in place that require operators to flare or incinerate gas during temporary activities and to search for opportunities to reduce their flaring and incinerating. The well completion by hydraulic fracturing requirements under the proposed Regulations would instead cover the rest of Canada, where similar provincial requirements are not in place.

Benefits and costs

Between 2018 and 2035, the cumulative GHG emission reductions attributable to the proposed Regulations are estimated to be approximately 282 Mt CO2e. Avoided climate change damages associated with these reductions are valued at $13.4 billion. The total cost of the proposed Regulations is estimated to be $3.3 billion, which would be offset in part by the recovery of 663 petajoules (PJ) (see footnote 13) of natural gas, with a market value of $1.6 billion, resulting in expected net benefits of $11.7 billion.

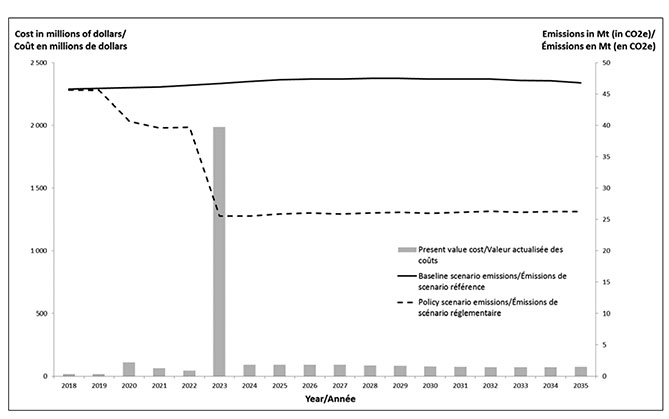

As shown in Figure 1 below, the most significant costs would be incurred in 2023, as standards requiring significant capital investment come into force. Beyond 2023, it is expected that emissions of methane would be reduced by more than 20 Mt (in CO2e) annually. In 2030, there would be net GHG emission reductions of about 20 Mt.

Figure 1: Baseline scenario and policy scenario methane emissions and compliance costs by year

Analytical framework

The impacts of the proposed Regulations have been assessed in accordance with the Treasury Board Secretariat (TBS) Canadian Cost-Benefit Analysis Guide. (see footnote 14) Regulatory impacts have been identified, quantified and, where possible, monetized.

The expected key impacts of the proposed Regulations are demonstrated in the logic model (Figure 2) below. Compliance with the proposed Regulations would result in incremental capital and operating costs for industry, and administrative costs for both industry and Government. Compliance would also result in reduced releases of natural gas (a mixture consisting of mostly methane), which would reduce GHG and volatile organic compound (VOC) (see footnote 15) releases to the atmosphere. Reductions in GHG emissions from the oil and gas sector would contribute towards mitigating climate change impacts. Reductions in VOCs would improve air quality which results in environmental and health co-benefits. Methane gas that would otherwise have been wasted through fugitive leaks or venting would now be flared or conserved as a potential energy source.

Figure 2: Logic model for the analysis of the proposed Regulations

Compliance with the Proposed Regulations |

→ | Reductions in GHG Emissions |

→ | Reduction in Climate Change Impacts |

→ | Social Benefits |

| → | Conserved Gas |

→ | Increased Productivity |

→ | ||

| → | Reductions in VOC Emissions |

→ | Improved Air Quality |

→ | ||

|

||||||

→ |

Compliance Costs |

→ |

Social Costs |

|||

Administrative Costs |

→ |

|||||

The analysis compares the expected incremental impacts of two scenarios: a baseline scenario and a regulatory scenario. The baseline scenario assumes a status quo in which the proposed Regulations are not implemented while the regulatory scenario assumes that the proposed Regulations are implemented. In addition, only existing provincial measures on limiting methane emissions originating from oil and gas facilities are considered in the analysis. All benefits and costs presented below are incremental to the baseline scenario, unless otherwise specified.

The time frame considered for this analysis is 2018 to 2035. The Department assumes the proposed Regulations would be published in the Canada Gazette, Part II, by the end of 2017. Thus, some early compliance by new facilities is expected beginning in 2018. Ongoing incremental costs and benefits following 2023 are estimated to be correlated with oil and gas production forecasts from the National Energy Board (NEB), which are available up to 2035. Benefits exceed costs in any given year beyond 2023. Therefore, the time frame for assessing impacts in this analysis is the 2018 to 2035 period (18 years), which is sufficient to fully demonstrate impacts and demonstrate whether or not the benefits of the proposed Regulations are likely to exceed the associated costs. A longer time period of analysis would show a larger net benefit because most of the costs of the proposed Regulations are upfront costs incurred in 2023, as shown in Figure 1 above.

The proposed Regulations contain five production, processing and transmission standards designed to reduce fugitive and vented emissions from upstream oil and gas producers. Leak detection and repair programs, well completion by hydraulic fracturing requirements and compressor limits would come into force in January 2020 while facility production venting requirements and emission limits for pneumatic controllers and pumps would come into force in January 2023.

All monetary results are shown in 2015 Canadian prices after inflating any non-2015 prices. When shown as present values, future year impacts have been discounted at 3% per year to 2016 (the year of the analysis), as per TBS guidance.

Analysis of regulatory coverage and compliance

To estimate the incremental benefits and costs of the proposed Regulations, the analysis considered who would be affected (regulatory coverage) and how they would most likely respond (their compliance strategies), as described below.

Regulatory coverage

The proposed Regulations would target emissions from the upstream oil and gas sector by implementing facility and equipment level requirements. Facility level requirements would include emission limits on facility production venting and LDAR standards. At the equipment level, there would be requirements for well completion by hydraulic fracturing, as well as limits on emissions from pneumatic devices (controllers and pumps) and compressors.

The proposed Regulations would cover facilities that have the potential to emit hydrocarbons above a 60 000 m3 per year threshold in any of the past five years and to facilities using equipment subject to the proposed standards (covered facilities). Currently, some facilities are expected to already meet the compliance requirements of the proposed Regulations, in part or completely, due to provincial measures. Facilities that would need to take incremental action to comply with the proposed Regulations are considered affected facilities. The cost-benefit analysis focuses on affected facilities when estimating incremental impacts of the proposed Regulations.

In order to estimate affected facilities in the oil and gas sector, upstream oil and gas facility numbers were obtained from Petrinex (Petroleum Information Network) (see footnote 16) for Alberta and Saskatchewan in 2012 and 2013, and forecasted using the production forecasts of crude oil and natural gas from the NEB. (see footnote 17) Due to limited available information, the number of facilities in the rest of Canada was forecasted using production to facility ratios calculated for Alberta and Saskatchewan. The Petrinex database was also used to determine and estimate the number of facilities in the oil and gas sector that would be covered by the proposed Regulations.

As mentioned above, the number of affected facilities that would require compliance action for each of the proposed standards was estimated using a combination of consultation and various consultant reports. (see footnote 18) The expected compliance strategies to be adopted by the oil and gas industry in order to meet the requirements for each standard under the proposed Regulations are described below.

Compliance with facility production venting requirements

The proposed Regulations would require covered facilities to limit vented gas to 3 000 m3 per year. Affected facilities would comply with the proposed Regulations either by destroying or conserving the gas. It is assumed that it would be less costly for a facility to conserve its vented gas if its gas production net of on-site fuel use is greater than 550 000 m3 per year. Also, if the facility is already selling more than 10 000 m3 of gas per year, it is assumed that it would conserve gas. If neither of the conditions are true, it is assumed the facility would destroy the gas by flaring.

Compliance with LDAR requirements

The proposed Regulations would require that a leak inspection take place three times a year for all covered facilities. As well, when a leak is detected, corrective action would be required to be taken and a reinspection would need to be done using a portable monitoring instrument.

Based on industry consultation, it is expected that in the baseline scenario, facilities in provinces without regulatory measures in place would perform LDAR about once every four years. In provinces with regulatory measures, gas plants are expected to perform LDAR every year, while all other facilities are expected to perform LDAR once every two years in the baseline scenario.

To comply with the proposed Regulations, affected facilities would perform LDAR three times a year. Facilities are assumed to hire a professional to conduct leak detection using an optical gas imaging (OGI) camera under the regulatory scenario. Should a leak be detected, a facility would be required to repair the leak and reinspect the leak using a portable monitoring instrument (a “sniffer”).

Compliance with the well completion by hydraulic fracturing requirements

The proposed Regulations would require new hydraulic fracturing or refracturing operations to conserve or destroy vented gas, except in British Columbia and Alberta (where provincial requirements exist). In the baseline scenario, it is expected that about 25% of covered wells are currently flaring emitted gas during this process while the rest are venting emitted gas. For the regulatory scenario, it is assumed that all hydraulic fracturing wells would flare emitted gases to comply with the proposed Regulations.

Compliance with pneumatic controller and pump requirements

The proposed Regulations would require affected facilities with pneumatic controllers to use low/no-bleed controllers, and affected facilities with pneumatic pumps to use electric pumps or pumps equipped with emissions control devices.

It is assumed that batteries (see footnote 19) and well sites would not have compressors that exceed the 745 kW threshold, so high-bleed pneumatic controllers would be replaced with low-bleed pneumatic controllers. As well, pneumatic pumps at batteries and well sites are assumed to be replaced with solar pumps.

Conversely, compressor stations and gas processing facilities are assumed to have compressors that exceed the 745 kW threshold. Pneumatic controllers would therefore need to be non-hydrocarbon emitting. These facilities are assumed to comply with the proposed Regulations by installing an air compressor and converting to air driven pneumatic controllers. Furthermore, these facilities are not expected to have pneumatic pumps requiring replacement, since the majority of pneumatic pumps are used at batteries and well sites.

For existing facilities, it is assumed that devices would be replaced in 2023. It is assumed that new facilities would purchase low-bleed controllers or solar pumps, beginning in 2018.

Compliance with compressor requirements

The proposed Regulations would set emission limits for both centrifugal and reciprocating compressors: 0.17 m3 per minute and 0.023 m3 per minute respectively. If the measurement exceeds the rate limit for the compressor type, corrective action must be taken and the rate of emissions must be measured again. In addition, any new compressors installed would be required to conserve vented gas.

It is expected that affected facilities with reciprocating compressors would replace rod packing every three years compared to replacement every five years in the baseline scenario to comply with the proposed standard. (see footnote 20) Affected facilities with centrifugal compressors are expected to install recovery systems on their wet seal degassing units to recover and reroute methane. (see footnote 21) The degassing recovery system would allow facilities with wet seals to forego retrofitting their compressors with dry seals and still mitigate methane emissions with little downtime.

| Standard | Year of Coming Into Force | Anticipated Compliance Action |

|---|---|---|

| LDAR | 2020 |

|

| Well completion by hydraulic fracturing requirements | 2020 |

|

| Compressors | 2020 |

|

| Facility production venting requirements | 2023 |

|

| Pneumatics | 2023 |

|

Industry costs of compliance by standard

Facilities covered by the proposed Regulations are expected to carry incremental capital and operating costs in order to comply with each standard. Both industry and the federal government are also expected to incur some administrative costs in order to ensure regulatory compliance.

Facility production venting compliance costs

Affected facilities are expected to either conserve the previously vented gas by installing a vapour recovery unit (VRU), or install a flare to destroy the gas. It is estimated that about 3 000 facilities would conserve gas, while about 4 000 facilities would flare it. Compliance costs borne by industry would include the operating costs associated with ongoing operation and management, and capital costs for VRU and flares. (see footnote 22) Capital costs are estimated at $150,000 to $200,000 per facility to purchase and install a VRU, and at $150,000 per facility to purchase and install a flare. Annual operating costs are estimated at $10,000 per facility to conserve gas, and at $5,000 per facility to flare. It is estimated that the facility production venting standard would result in a cost to industry of $1,201 million between 2018 and 2035.

LDAR compliance costs

The proposed Regulations would require affected facilities to undertake leak detection more frequently than they otherwise would have in the baseline scenario. It is estimated that about 42 000 facilities would be covered by the LDAR requirements. Compliance costs to industry would include the capital cost of putting in place an LDAR data collection system of $21,000 per facility. As well, costs would be incurred to detect leaks using OGI equipment (through the hiring of a professional). (see footnote 23) The number of components per facility is used to estimate the time it would take a consultant to conduct OGI leak detection, assumed to cost $190 an hour, which includes the wage paid to the consultant plus the rental rate for the camera. Upon completion of a repair, the proposed Regulations require that the repaired leak be inspected using a portable monitoring instrument (a “sniffer”) in accordance with the U.S. Environmental Protection Agency Method 21. Per component, the cost of inspection (with an OGI camera) and reinspection (with a sniffer) is estimated to be 43 cents. (see footnote 24) It is estimated that the LDAR standard would result in a cost to industry of $374 million between 2018 and 2035.

The analysis assumes that leaks are random and independent events and that new leaks are unlikely to reoccur within the baseline reinspection period (up to four years). Therefore, the number of leaks that are detected is essentially the same (change of less than 1%) in the baseline and regulatory scenarios. Under the regulatory scenario, leaks would, however, be detected earlier than they would in the baseline scenario. As a result, the analysis has not considered the incremental cost of repairs.

Well completion by hydraulic fracturing requirements compliance costs

The analysis assumes that under the regulatory scenario, all affected fracturing and refracturing wells would flare emitted gases. It is estimated that about 15 000 oil and gas wells would be required to install a flare over the time frame of the analysis. It is expected that flaring well completion emissions would cost $4,000 (flares required for well completions are generally rented on a temporary basis and are therefore less costly than facility flaring described above). (see footnote 25) It is estimated that this standard would result in a cost to industry of $41 million between 2018 and 2035.

Pneumatic controllers and pumps compliance costs

The analysis calculates the number of pneumatic devices affected by multiplying the number of affected facilities by an estimated number of devices per facility. (see footnote 26) The analysis assumes that new facilities would carry the incremental cost difference between a high-bleed device and a compliant device, while existing facilities would carry the full cost of a new device.

It is estimated that the number of gas-driven pneumatic devices per facility would range between 0 and 18 for most facilities. (see footnote 27) Compliance costs to industry would consist of the incremental capital and labour cost of replacement or retrofit ranging from $0 to $917 for new facilities, and $276 to $2,348 for existing facilities. At compressor stations and gas processing facilities, it is expected that an air compressor would be installed to convert existing devices to be air driven. This is estimated to cost $65,000 per facility. (see footnote 28) For pneumatic pumps, it is assumed that facilities would replace pumps with solar pumps, which is estimated to cost $7,500 for new facilities and $16,200 for existing facilities. (see footnote 29) It is estimated that the pneumatics standard would result in a cost to industry of $1,492 million between 2018 and 2035.

Compressors compliance costs

Facilities with reciprocating compressors would replace rod packing more frequently as a result of the proposed Regulations. It is estimated that the rod packing would need to be replaced more frequently for about 9 000 reciprocating compressors, and the incremental cost to replace the rod packing for a reciprocating compressor more frequently is estimated at an annualized cost of $300. In addition, approximately 1 500 newly installed reciprocating compressors would be required to capture all emitted gases. (see footnote 30) The estimated cost to install conservation equipment would be about $27,000 per compressor.

Facilities with centrifugal compressors are expected to augment their compressors with a recovery unit that conserves the gas vented from the compressor's wet seal degassing system. It is estimated that there are around 90 affected centrifugal compressors, and the cost of installing a wet seal degassing system is estimated to be $45,000. It is estimated that the compressor standard would result in a cost to industry of $157 million between 2018 and 2035.

Summary of industry compliance costs

Compliance costs associated with the proposed Regulations would increase the marginal cost of producing natural gas (and other fuels) in Canada. With no offsetting effects, these incremental costs are expected to decrease the quantity of natural gas produced in Canada, relative to the baseline scenario. Given the integrated nature of the North American market for natural gas, it is assumed that these decreased quantities would be replaced by imported natural gas. (see footnote 31) For the purposes of this analysis, industry compliance costs of $3.3 billion (see Table 2) are used as a proxy for the value of this compliance cost effect. These compliance costs would be offset, in part, by the recovery of 663 PJ of natural gas with a market value of $1.6 billion, described in the benefits analysis below.

| Proposed Standard | 2018–2025 | 2026–2030 | 2031–2035 | Total |

|---|---|---|---|---|

| Facility production venting requirements | 749 | 229 | 222 | 1,201 |

| Leak detection and repairs | 187 | 102 | 85 | 374 |

| Well completion requirements | 16 | 17 | 8 | 41 |

| Pneumatic controllers and pumps | 1,411 | 53 | 28 | 1,492 |

| Compressors | 74 | 45 | 38 | 157 |

| Total | 2,437 | 446 | 381 | 3,265 |

Note: Numbers may not add up due to rounding. Monetized values are discounted to present value using a 3% discount rate.

Most of the compliance costs are expected to occur in 2023 (about $2.0 billion as shown in Figure 1 above), when the facility production venting, and pneumatic device and pump requirements come into effect.

Industry and government administrative costs to ensure compliance

Presently, there are no federal regulations established to regulate GHG emissions in the oil and gas sector. The proposed Regulations would require regulatees to register facilities, keep records, and submit registration and compliance reports. These industry administrative costs are estimated to be $21 million between 2018 and 2035. (see footnote 32)

The Department would also incur costs to enforce the proposed Regulations, conduct compliance promotion and administer the proposed Regulations. In 2018, an estimated one-time cost of about $209,000 is expected to be required for the training of enforcement officers and $50,000 to meet information management requirements. The annual inspection cost is estimated to be $571,500. This cost includes inspections, investigations, measures to deal with alleged violations and prosecutions and is estimated to be $8 million between 2018 and 2035.

Compliance promotion activities are intended to encourage the regulated community to achieve compliance. Compliance promotion costs include distributing the proposed Regulations, developing and distributing promotional materials (such as a fact sheet and web material), advertising in trade and association magazines and attending trade association conferences. This cost is estimated to be $148,000 between 2018 and 2022.

The proposed Regulations allow for a temporary permitted exemption for facilities where meeting the requirements for pneumatic pumps would be technically or economically infeasible. These permits would need to be reviewed and approved by the Government of Canada. The total cost of permit reviews is estimated to be $35,000 between 2018 and 2035.

Table 3 below summarizes the administrative cost to ensure compliance for both industry and Government.

| 2018–2025 | 2026–2030 | 2031–2035 | Total | |

|---|---|---|---|---|

| Industry administrative costs | 11 | 6 | 5 | 21 |

| Government administrative costs | 5 | 2 | 2 | 8 |

| Total administrative costs | 15 | 8 | 7 | 29 |

Note: Numbers may not add up due to rounding. Monetized values are discounted to present value using a 3% discount rate.

Administrative costs to industry and Government necessary to ensure compliance are estimated to be $29 million between 2018 and 2035.

Benefits of regulatory coverage and compliance

The proposed Regulations would reduce vented and fugitive emissions of methane, a potent GHG, through the requirements to conserve fugitive and vented natural gas. This means that natural gas that would otherwise have been wasted would be conserved as a potential energy source. In addition, emissions of VOCs would be reduced, leading to improved air quality, which can improve the environment and health of Canadians.

To monetize the benefits, the social cost of carbon (SCC) has been applied to the CO2 emission reductions, and the social cost of methane (SCCH4) has been applied to the methane (CH4) emission reductions to value the avoided climate change damages resulting from reductions in GHG emissions. A market price for natural gas has been applied to value the amount of gas conserved.

Given the resource-intensive and time-consuming nature of air quality modelling, the Department is still in the process of finalizing air quality modelling results for reductions in VOCs. Therefore, VOC emissions reductions have not been monetized for this analysis.

Quantification of benefits

The analysis estimated the conserved gas and quantified the emission reductions by first developing detailed engineering emissions estimates for each proposed standard, and then scaling these to the Department's overall emission estimates for the oil and gas sector in order to ensure that the estimates are consistent.

To calculate natural gas reductions, natural gas emission factors for the various standards and product types were multiplied by the total number of devices for the respective standard. This procedure calculates the total amount of natural gas that would be recovered by implementing the proposed Regulations. The difference between the emissions in the baseline scenario and the emissions in the regulatory scenario were used to estimate the incremental reductions.

The sources for the emission factors differ for each standard

- — For facility production venting requirements, provincial data on facility venting and flaring volumes were used to estimate the baseline emissions, and compared to the required reductions as per the proposed Regulations;

- — For LDAR, the emission factors for the policy scenario are obtained using the methods from the 1995 U.S. EPA Protocol and applying factors from an engineering assessment of fugitive equipment leak emission factors undertaken in 2014; (see footnote 33), (see footnote 34)

- — For well completion by hydraulic fracturing requirements, emission factors are obtained from the U.S. EPA; (see footnote 35)

- — For pneumatic devices, emission factors were derived from an engineering assessment of pneumatic devices undertaken in British Columbia in 2013; (see footnote 36) and

- — For compressors, the emission factors for the reciprocating compressors are estimated using the Environmental Defense Fund (EDF) sawtooth method. (see footnote 37) The EDF study provided a start and end emission factor which increases linearly to produce a timeline of emission based on months passed since the last rod packing change. For centrifugal compressors, the emission factors are obtained from an engineering assessment of compressors undertaken in 2014 by the U.S. EPA. (see footnote 38)

To separate emissions of natural gas into the different pollutants, the composition of emitted and conserved natural gas is determined using estimates of gas composition from the Clearstone Engineering report, (see footnote 39) with the exception of gas from facility production venting, as these composition ratios were obtained from a combination of reports from provinces. (see footnote 40) To obtain the amounts of CO2, CH4 or VOCs reduced, the natural gas reductions are multiplied by the composition ratios for each standard which are provided in Table 4 below.

| Standard | Product Type | CO2 | CH4 | VOCs |

|---|---|---|---|---|

| Venting | Light oil | 10% | 53% | 22% |

| Venting | Heavy oil | 6% | 89% | 2% |

| Venting | Cold heavy oil with sand | 2% | 94% | 1% |

| All others | Light oil | 1% | 84% | 4% |

| All others | Heavy oil | 1% | 84% | 4% |

| All others | Non-associated gas | 2% | 88% | 5% |

| All others | Tight gas | >1% | 94% | 2% |

| All others | Shale gas | >1% | 94% | 2% |

| All others | Coal bed methane gas | >1% | 96% | 1% |

| All others | Gas processing | 2% | 88% | 5% |

The engineering emission estimates were then scaled to align with the departmental baseline emissions forecasts. The departmental baseline emission projections for the oil and gas sector are determined using the production forecast of oil and gas from the NEB, in combination with the national inventory report. These departmental projections are developed in the Energy, Emissions and Economy model (E3MC), one of the Department's models for estimating GHG emission trends and policy impacts in Canada. This analysis uses emissions projections as reported in Canada's Second Biennial Report on Climate Change to United Nations Framework Convention on Climate Change. (see footnote 41)

The baseline engineering emission estimates were compared to the departmental baseline emission forecast to obtain a ratio or scaling factor. This scaling factor was applied to the engineering estimates to derive final incremental emission reduction estimates for the proposed Regulations. The scaling factor is broken down by province, by sector, and by pollutant (CH4, CO2 and VOC), but not by emission source. Further scaling was done where necessary to ensure that incremental reductions do not exceed baseline emission estimates.

Greenhouse gases emission reductions

The proposed Regulations would reduce methane emissions that would be emitted into the atmosphere. At the same time, the proposed Regulations are estimated to result in a slight increase in flaring activities, which would slightly increase CO2 emissions. The proposed Regulations would reduce 12 Mt of methane emissions over the time frame of analysis. Using a global warming potential factor of 25, the decrease in methane emissions is estimated at 295 Mt CO2e between 2018 and 2035. The increase in CO2 as a result of the increase in flaring activities is estimated to be 14 Mt over the time frame of analysis.

The net GHG emission reductions are measured as the combined reductions of CH4 and CO2, as well as the increase in CO2 emissions from increased flaring. It is estimated that a net 282 Mt CO2e of GHG emissions would be reduced between 2018 and 2035 as a result of the proposed Regulations as seen in the table below.

| Proposed Standard | Net GHGs (CH4 + CO2) | CH4 | CO2 | |||

|---|---|---|---|---|---|---|

| 2018–2025 | 2026–2030 | 2031–2035 | 2018–2035 | 2018–2035 | 2018–2035 | |

| Facility production venting requirements | 26 | 44 | 42 | 112 | 125 | –13 |

| Leak detection and repairs | 23 | 20 | 20 | 64 | 64 | 0 |

| Well completion requirements | 2 | 1 | 1 | 4 | 5 | –1 |

| Pneumatic controllers and pumps | 19 | 27 | 26 | 72 | 72 | 0 |

| Compressors | 9 | 10 | 11 | 30 | 30 | 0 |

| Total | 80 | 102 | 100 | 282 | 295 | –14 |

Note: Numbers may not add up due to rounding. CO2 emissions increase as a result of facilities flaring vented gas. Methane (CH4) emissions are presented in Mt CO2e, which is calculated by multiplying methane emission reductions by a global warming potential of 25.

The impacts of reducing GHG emissions in the atmosphere were valued using the departmental SCCH4 and SCC. (see footnote 42) The SCCH4 and SCC represent estimates of the economic value of avoided climate change damages at the global level for current and future generations (from present day to 2300) as a result of reducing CH4 and CO2 emissions over the time frame of analysis (2018–2035).

In 2018, the SCC and SCCH4 are estimated at $44 and $1,273 respectively, whereas in 2035, the SCC and SSCH4 are estimated at $61 and $2,026. Over the time frame of analysis, the SCCH4 is applied to 12 Mt of methane reductions and the SCC is applied to 14 Mt increase in CO2 as a result of flaring. The present value of the reduction of GHGs is around $13.4 billion.

| Proposed Standard | 2018–2025 | 2026–2030 | 2031–2035 | Total |

|---|---|---|---|---|

| Facility production venting requirements | 1,283 | 2,117 | 2,017 | 5,417 |

| Leak detection and repairs | 1,118 | 950 | 944 | 3,012 |

| Well completion by hydraulic fracturing requirements | 78 | 71 | 41 | 189 |

| Pneumatic controllers and pumps | 927 | 1,280 | 1,198 | 3,405 |

| Compressors | 453 | 455 | 497 | 1,406 |

| Total | 3,858 | 4,873 | 4,697 | 13,429 |

Note: Numbers may not add up due to rounding. Monetized values are discounted to present value using a 3% discount rate. The SCCH4 is applied to the reduction of methane emissions while the SCC is applied to the increase in CO2 emissions.

It is expected that the proposed Regulations would lead to a 21 Mt reduction in methane emissions in 2025, a reduction of 41% below 2012 levels, falling in the range of a 40% to 45% reduction as committed in March 2016. It is also expected that the proposed Regulations would lead to a 20 Mt reduction in net GHG emissions in 2030, an estimated 7% contribution to Canada's GHG emissions reduction target under the Paris Agreement.

Conserved gas

Methane is the primary component in natural gas, which can be used as a source of energy for heating, cooking, and electricity generation. Technical and process changes required by the proposed Regulations would result in more efficient operations, with limited methane venting, reduced leakage, and the conservation of approximately 663 PJ of natural gas (see Table 7). This improved efficiency would increase the marginal productivity of natural gas production, and to some extent offset the industry compliance costs described above. It would also increase the quantity of natural gas produced in Canada, and displace imported supply. (see footnote 43) Given that recovered natural gas has already been extracted, and that the costs associated with its recovery were accounted for in the industry compliance costs, the full market value of this recovered natural gas is assumed to be a reasonable proxy for the value of this conserved resource. The conservation of VOCs has not been quantified due to the relatively small quantities and the variability of hydrocarbon make-up of these VOCs.

| Proposed Standard | 2018–2025 | 2026–2030 | 2031–2035 | Total |

|---|---|---|---|---|

| Facility production venting requirements | 69 | 115 | 112 | 295 |

| Leak detection and repairs | 52 | 45 | 45 | 141 |

| Well completion by hydraulic fracturing requirements | 0 | 0 | 0 | 0 |

| Pneumatic controllers and pumps | 43 | 60 | 57 | 160 |

| Compressors | 21 | 21 | 24 | 66 |

| Total conserved gas | 184 | 241 | 238 | 663 |

Note: Numbers may not add up due to rounding.

A market price for natural gas was used to estimate what companies are willing to pay for conserved resources. Estimates of future Alberta Energy Company natural gas prices (AECO-C) were calculated using the Henry Hub natural gas price forecasted by the NEB and subtracting $0.65/gigajoule (GJ) to reflect historic spreads between the two prices. (see footnote 44) This price forecast, ranging from $2.43/GJ in 2018 to $3.68/GJ in 2035, was then applied to the estimated quantity of methane that would be conserved. The value of conserved gas as a result of the proposed Regulations is estimated to be $1.6 billion over the time frame of the analysis (see Table 8). (see footnote 45) This market price estimate may overvalue society's willingness to pay to conserve natural gas, an uncertainty that has been considered in the sensitivity analysis below.

| Proposed Standard | 2018–2025 | 2026–2030 | 2031–2035 | Total |

|---|---|---|---|---|

| Facility production venting requirements | 178 | 280 | 245 | 702 |

| Leak detection and repairs | 134 | 109 | 99 | 341 |

| Well completion requirements | 0 | 0 | 0 | 0 |

| Pneumatic controllers and pumps | 111 | 146 | 125 | 383 |

| Compressors | 54 | 52 | 52 | 158 |

| Total value of conserved gas | 478 | 586 | 521 | 1,585 |

Note: Numbers may not add up due to rounding. Monetized values are discounted to present value using a 3% discount rate.

Volatile organic compounds

The proposed Regulations, through reductions of fugitive and venting emissions, would also reduce by up to 769 kt the quantity of VOCs that would enter the atmosphere over the time frame of analysis.

| Proposed Standards | 2018–2025 | 2026–2030 | 2031–2035 | Total |

|---|---|---|---|---|

| Facility production venting requirements | 115 | 208 | 217 | 541 |

| Leak detection and repairs | 33 | 29 | 30 | 91 |

| Well completion requirements | 3 | 3 | 2 | 8 |

| Pneumatic controllers and pumps | 25 | 36 | 35 | 96 |

| Compressors | 9 | 11 | 13 | 33 |

| Total VOC reductions | 186 | 286 | 297 | 769 |

Note: Numbers may not add up due to rounding.

VOCs contribute to the formation of ground level ozone and particulate matter, which are the main constituents of smog. Smog is known to have adverse effects on human health and the environment. The Department uses the following three different models to estimate the health and environmental impacts of air pollution: a model to estimate VOC emission impacts on air quality; a model to estimate health impacts associated with the changes in air quality; and a model to estimate environmental impacts associated with the changes in air quality. Given the resource-intensive and time-consuming nature of air quality modelling, the Department is still in the process of finalizing the modelling results. Thus, monetized health and environmental benefits attributable to VOC reductions are not available at this time, but are planned to be presented in the analysis for publication in the Canada Gazette, Part II.

Summary of benefits and costs

The proposed Regulations are expected to achieve 282 Mt CO2e in GHG emission reductions, 663 PJ of conserved gas and 769 kt of VOC emission reductions, as shown in Table 10 below. These quantitative benefits have been monetized where possible, or assessed as qualitative benefits.

By 2035, the proposed Regulations are estimated to result in cumulative net GHG emission reductions of 282 Mt, valued at around $13.4 billion, and cumulative gas conserved of 663 PJ, valued at around $1.6 billion. The total benefits of the proposed Regulations are valued at around $15.0 billion. The proposed Regulations would also result in costs to industry and government of $3.3 billion. The net benefits of the proposed Regulations for Canadians are $11.7 billion. These costs and benefits associated with the proposed Regulations are summarized in Table 10.

| Monetized Impacts (millions of dollars) | 2018–2025 | 2026–2030 | 2031–2035 | Total |

|---|---|---|---|---|

| Climate change benefits | 3,858 | 4,873 | 4,697 | 13,429 |

| Value of conserved gas | 477 | 586 | 521 | 1,585 |

| Total benefits | 4,336 | 5,460 | 5,218 | 15,014 |

| Industry compliance costs | 2,437 | 446 | 381 | 3,265 |

| Industry administrative costs | 11 | 6 | 5 | 21 |

| Government administrative costs | 5 | 2 | 2 | 8 |

| Total costs | 2,453 | 454 | 389 | 3,295 |

| Net benefits | 1,883 | 5,006 | 4,895 | 11,719 |

| Quantified benefits | ||||

| Net GHG reduction (Mt CO2e) | 80 | 102 | 100 | 282 |

| Gas conserved (PJ) | 184 | 241 | 238 | 663 |

| VOC reduction (kt) | 186 | 286 | 297 | 769 |

| Qualitative benefits | ||||

| Health and environmental benefits due to VOC emission reductions. | ||||

Note: Numbers may not add up due to rounding. Monetized values are discounted to present value using a 3% discount rate.

The proposed Regulations are expected to achieve a net 182 Mt CO2e cumulative reduction in GHG emission reductions by 2030, which would contribute to addressing Canada's international commitments, including the 2015 Paris Agreement. To achieve these GHG emission reductions, it is expected that compliance costs of $2.9 billion would be incurred. However, conserved gas valued at $1.1 billion over the same time frame (2018–2030) is also expected. Overall, as indicated in Table 11, the anticipated GHG emission reductions would be achieved at an estimated cost per tonne of $16, and a net cost per tonne of about $10.

| Type of Cost per Tonne | Costs (millions of dollars) |

GHG Emission Reductions (Mt CO2e) |

Cost per Tonne |

|---|---|---|---|

| Cost per tonne | 2,900 | 182 | 16 |

| Net cost per tonne | 1,800 | 182 | 10 |

Note: Monetized values are discounted to present value using a 3% discount rate.

These costs per tonne results reflect expected compliance costs and conserved gas savings to reduce tonnes of GHG emissions from methane. These results do not account for when emission reductions occur, or for the value society may place on the avoided damages.

Distributional analysis of regulatory impacts

This summary presents the benefits and costs to Canadian society as whole. These impacts are not uniformly distributed across society so the analysis has considered a range of distributional impacts.

Impacts by region

The compliance costs associated with the proposed Regulations would vary by region. The production of oil and gas is mainly concentrated in the provinces of British Columbia (B.C.), Alberta (Alta.), and Saskatchewan (Sask.). Table 12 shows the breakdown of overall costs, emission reductions, and conserved gas attributable to the proposed Regulations across Canadian regions. As expected, due to the concentration of oil and gas activities in the Western provinces, the major impacts are expected in British Columbia, Alberta, and Saskatchewan with the remainder distributed throughout the rest of Canada (ROC).

| Category | B.C. | Alta. | Sask. | ROC | Total |

|---|---|---|---|---|---|

| Reduced net GHG emissions (Mt CO2e) | 19 | 183 | 77 | 3 | 282 |

| Gas conserved (PJ) | 43 | 433 | 180 | 7 | 663 |

| Reduced VOC emissions (kt) | 35 | 560 | 168 | 5 | 769 |

| Compliance costs (million $) | 238 | 2,293 | 715 | 19 | 3,265 |

Note: Numbers may not add up due to rounding. Monetized values are discounted to present value using a 3% discount rate.

Impacts by product

The compliance costs associated with the proposed Regulations would also vary by product. Table 13 shows the breakdown of overall costs and benefits of the proposed Regulations across oil and gas products. Due to the large number of facilities affected, the natural gas production and processing sector is expected to incur the largest cumulative costs and attributed emission reductions over the period of analysis.

| Category | Light Oil | Heavy Oil | Natural Gas | Total |

|---|---|---|---|---|

| Reduced net GHG emissions (Mt CO2e) | 59 | 99 | 124 | 282 |

| Gas conserved (PJ) | 147 | 241 | 275 | 663 |

| Reduced VOC emissions (kt) | 562 | 51 | 156 | 769 |

| Compliance costs (million $) | 1,014 | 546 | 1,706 | 3,265 |

Note: Numbers may not add up due to rounding. Monetized values are discounted to present value using a 3% discount rate.

Consumer impacts

Given that crude oil and natural gas are commodities which are priced in global and continental markets, the proposed Regulations are not expected to have any impacts on the price of these products. Thus, the proposed Regulations are not expected to have any impacts on consumers.

Competitiveness impacts

The proposed Regulations would impose compliance costs on oil and gas companies, which would divert resources from other productive uses. The impacts of the costs of regulatory compliance would likely be greater for firms with constrained access to capital, such as smaller oil and gas producers with lower levels of production.

The Department anticipates that the impact of the proposed Regulations would likely be small for producers of light oil and natural gas. It is expected that heavy oil producers would experience slightly higher financial impacts, because compliance costs represent a larger proportion of their current development costs relative to natural gas and light oil wells. As a consequence of the cost difference, heavy oil wells have a greater proportional impact on profitability.

Total compliance costs are estimated to be $3.3 billion over the period of analysis. In 2015, total capital and operating expenditures in the Western Canadian conventional oil and gas sector were $52 billion, the lowest level since 2009 and 3% lower than the average annual expenditures over the previous 10 years. If spending in the sector remained at these comparatively low levels over the time frame of analysis, the compliance costs from the proposed Regulations would represent around 0.5% of cumulative industry expenditures ($700 billion) over the 18-year period.

For existing facilities, the costs of compliance can represent large one-time expenses. Some investments could be influenced at the margin and these costs could affect the viability of facilities with lower production if they do not have sufficient time remaining in the facility's life to recover the compliance costs. In certain cases, existing facilities may cease production earlier than they otherwise would have in the absence of the proposed Regulations.

In response to the potential financial and competitiveness impacts of the proposed Regulations, several flexibilities have been included. For example, standards that would require significant capital investment, such as the facility production venting requirements and the pneumatic controller and pump requirements, would not come into force until 2023, giving firms lead time to adjust. The proposed Regulations would also allow facilities that experience technical or economic challenges from complying with the standard for pneumatic pumps to apply for a time-limited exemption permit.

Potential competitiveness concerns posed by the proposed Regulations could be further offset by existing regulations in the United States and commitments from Mexico. The proposed Regulations are based on current U.S. source-by-source rules that apply to new and modified oil and gas facilities, which were finalized in 2012 and 2016.

Uncertainty of impact estimates

The discount rate used for this analysis is 3%, as recommended by TBS for environmental and health projects. TBS also recommends using a 7% discount rate for other cost-benefit analyses. A sensitivity analysis comparing the central case (3%) to a higher discount rate (7%) still yields an expected net benefit, as shown in Table 14.

Uncertainty is also associated with the values used to monetize the benefits from GHG emission reductions. For example, the central SCC value used in this cost-benefit analysis may not fully capture potential low-probability, high-impact outcomes due to climate change. To address this concern, the Department publishes a 95th percentile SCC value for sensitivity analyses, which attempts to capture the costs associated with low-probability, high-impact outcomes, including potential catastrophic impacts of climate change.

It is also possible that costs are higher than estimated and benefits are lower than estimated (e.g. if the value of conserved gas is significantly lower than the market price of natural gas), which would lower the estimated net benefits. Over the analysis time frame, estimated benefits were almost five times greater than costs (a benefit-to-cost ratio of 5:1). Thus, even if benefits were nearly five times smaller or costs were nearly five times larger than estimated, there would still be an expected net benefit. The Department has typically considered uncertainty ranges 50% higher or lower than the central case. Sensitivity analyses that considered these scenarios still yield expected net benefits, as shown in Table 14 below.

| Alternate Impact Analysis Estimates | Benefits (B) |

Costs (C) |

Net Benefits (B – C) |

Benefit-Cost Ratio (B/C) |

|---|---|---|---|---|

| Central case (from table 11) | 15,014 | 3,295 | 11,728 | 5:1 |

| Benefits and costs discounted at 7% per year | 9,488 | 2,384 | 7,104 | 4:1 |

| GHGs valued using 95th percentile SCC/SCCH4 | 43,666 | 3,295 | 40,371 | 13:1 |

| Reduced conserved gas benefit | 13,429 | 3,295 | 10,134 | 4:1 |

| Benefits 50% lower and costs 50% higher | 7,507 | 4,927 | 2,580 | 2:1 |

Note: Values discounted to present value using a 3% discount rate, except in the case in which a 7% rate is used.

It is assumed that the impacts (benefits and costs) occur because regulatees would not change their behaviour in the absence of the proposed Regulations. There could be some “natural adoption” of lower-emitting equipment or practice without the proposed Regulations. If an alternate baseline scenario had been proposed whereby more regulatees would have chosen these GHG reduction strategies voluntarily, then the estimated costs and benefits attributable to the proposed Regulations would be proportionally lower, which would still yield an expected net benefit.

“One-for-One” Rule

The proposed Regulations are considered an “IN” under the Government of Canada's “One-for-One” Rule. The total annualized administrative costs for the regulatees to comply with the regulatory requirements over a 10-year time frame would be approximately $1.1 million for all stakeholders, or $1,100 per company. (see footnote 46) In addition, the proposed Regulations would be a new regulatory title (IN), which must be offset by the repeal of an existing regulation (OUT) under the Government of Canada's “One-for-One” Rule.

The main driver (78%) of administrative costs is record keeping, as facilities would be required to keep records of compliance. It is assumed that some of the data needed to comply with this requirement is already accessible and kept by the regulatees in British Columbia, Alberta and Saskatchewan, due to existing provincial requirements. Consequently, the additional information that is required is mainly the record keeping of emissions of methane from the facility and the leak incidences. This is estimated to range from 15 minutes to 40 hours per company per year depending on the standard. (see footnote 47)

The other main driver (17%) of administrative costs is facility registration requirements. For each facility, regulatees would be required to register and send to the Minister a one-time registration report. Based on the data used for recently published regulations affecting the oil and gas sector, it is assumed that it takes 1.5 hours to register each facility and 2 hours per company to prepare and submit the information. (see footnote 48)

Small business lens

It is estimated that the proposed Regulations would affect 57 874 oil and gas facilities, owned by 1 062 companies. Although the majority of facilities that would be covered by the proposed Regulations are owned by medium and large businesses, some facilities operated by small businesses would also be covered. Therefore, the proposed Regulations would trigger the small business lens. An estimated 579 facilities are owned by 475 small businesses.

To reduce costs associated with the proposed Regulations for small businesses, several regulatory design elements would be incorporated into the proposed Regulations (flexible option). Facilities operating with a potential to emit (PTE) under the 60 000 m3 threshold would be exempt from most of the facility-based requirements under the proposed Regulations. Since most small businesses own facilities that emit gaseous hydrocarbons less than the threshold, they would not be subject to the above-mentioned requirements, nor the associated record-keeping and reporting requirements. The proposed Regulations are expected to impact only about 23% of small businesses. The Regulatory Flexibility Analysis Statement below (table 15) shows the expected costs to small businesses under the initial and flexible options.

| Initial Option (standards without a 60 000 m3 PTE threshold) |

Flexible Option (standards with a 60 000 m3 PTE threshold) |

|||

|---|---|---|---|---|

| Number of small businesses impacted | 475 | 475 | ||

| Annualized Value (see footnote *) | Present Value | Annualized Value (see footnote **) | Present Value | |

| Compliance costs | $5,284,000 | $69,566,000 | $997,000 | $13,126,000 |

| Administrative costs | $128,000 | $1,691,000 | $73,000 | $963,000 |

| Total costs | $5,412,000 | $71,257,000 | $1,070,000 | $14,089,000 |

| Total cost per small business | $11,000 | $150,000 | $2,000 | $30,000 |

| Risk considerations:

The initial option would cover all facilities, including small facilities which, in total, account for a small portion of the emissions. The initial option would impose a relatively higher cost (relative to production/revenues) on smaller facilities than on larger facilities. In the oil and gas sector, it is typical for a small business to be operating facilities that fall under the threshold for application in the flexible option. These facilities do not represent a significant portion of the total emissions. The proposed Regulations cover the majority of emissions while providing flexibility for small businesses. |

||||

Overall, the flexible option results in an estimated reduction of total costs per small business of about $120,000 between 2018 and 2035 relative to the initial option under consideration, or about $9,000 per year. The proposed Regulations would result in cumulative costs of about $14 million for small businesses, or $30,000 per small business. While not part of this assessment, the design elements of the flexible option are expected to also reduce administrative and compliance costs for large businesses that own smaller facilities.

Consultation

Since April 2016, the Department has held over 150 hours of consultations with stakeholders and provincial partners on the proposed Regulations, including webinars, teleconferences, face-to-face meetings, technical discussions and bilateral meetings. Representatives from industry, provinces, territories, environmental non-governmental organizations (ENGOs) and associations representing Indigenous peoples have participated.

The Department presented to stakeholders and provincial partners a description of a draft regulatory approach early in the consultation process, which included proposals to manage five emission sources using regulation, specific emission limits for significant emission sources, and anticipated compliance actions that could reduce methane emissions from each source. Three operational control measures (LDAR, compressors and well completions) were proposed to come into force in 2018, while two control measures requiring more substantial capital investment (facility venting limits and pneumatic device venting restrictions) were proposed to come into force in 2020. The proposed Regulations reflect feedback on this approach, ranging from broad changes in the timing of coming into force to requirements pertaining to specific emission sources.

Industry